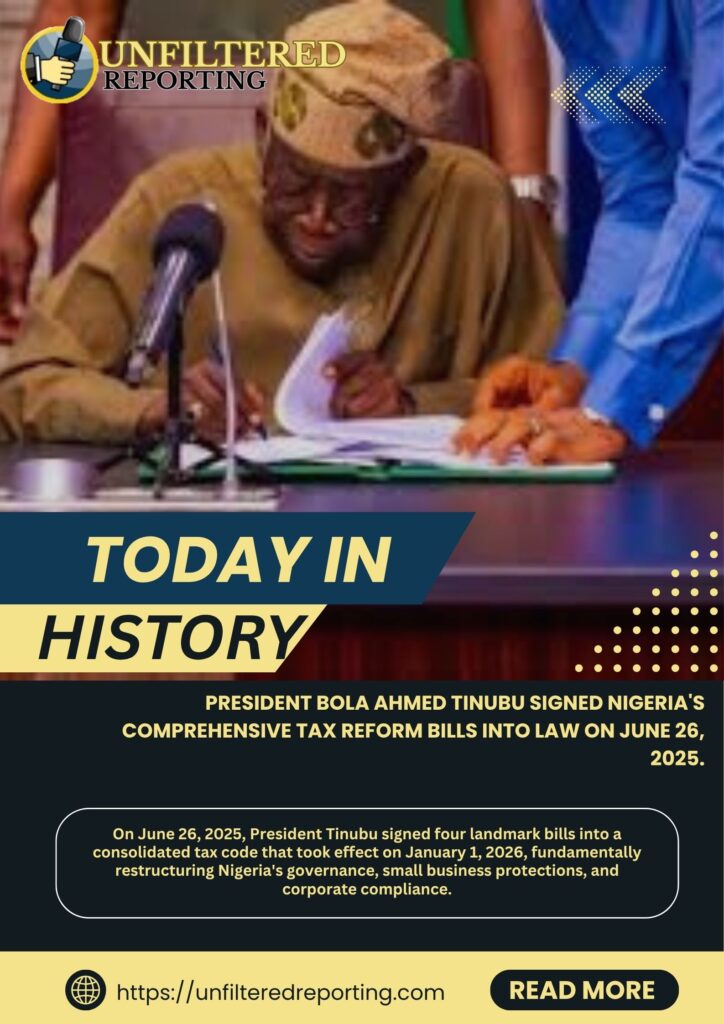

Today in History: Inside Nigeria’s Comprehensive Tax Reform Acts

On Thursday, June 26, 2025, President Bola Ahmed Tinubu signed a bill into law that fundamentally altered the economic landscape of Nigeria. By granting presidential assent to four tax reform bills on that historic day, the administration effectively dismantled decades of fragmented, overlapping fiscal laws and replaced them with a consolidated, modern tax code. Developed in tandem with the Presidential Fiscal Policy and Tax Reforms Committee; these laws formally took effect on January 1, 2026. This landmark legislative shift is restructuring governance, protecting small businesses, and redefining corporate compliance across Nigeria.

Instead of navigating a maze of disconnected statutes, taxpayers and authorities now operate under four distinct, synchronized Acts.

The Nigeria Tax Act (NTA) serves as the structural core, repealing and amalgamating over a dozen legacy laws including the Companies Income Tax Act (CITA), Personal Income Tax Act (PITA), Value Added Tax (VAT) Act, and Capital Gains Tax Act (CGTA) into a singular, unified statute.

The Nigeria Tax Administration Act (NTAA) introduces a single procedural framework for how taxes are assessed, collected, and enforced across federal, state, and local governments, removing administrative friction.

The Nigeria Revenue Service (Establishment) Act (NRSA) officially rebrands and restructures the Federal Inland Revenue Service (FIRS) into the Nigeria Revenue Service (NRS), granting it enhanced digital collection capabilities and a broadened mandate to oversee both tax and non-tax revenues.

The Joint Revenue Board (Establishment) Act (JRBA) harmonizes intergovernmental tax policies to prevent multiple taxation, while creating the independent Office of the Tax Ombudsman to safeguard taxpayer rights.

A core philosophy of the reforms signed on June 26, 2025, is shifting the tax burden away from the vulnerable and micro-businesses toward higher earners and major corporations.

The reform effectively shields Micro, Small, and Medium Enterprises (MSMEs) by dramatically adjusting the criteria for tax exemptions. Small companies are now defined as those with an annual gross turnover of ₦100 million or less (a major leap from the previous ₦25 million ceiling) and fixed assets not exceeding ₦250 million. These entities are now completely exempt from Companies Income Tax (CIT), Capital Gains Tax (CGT), and the newly minted Development Levy.

Personal Income Tax (PIT) has been restructured into a highly progressive framework designed to alleviate cost-of-living pressures. Individuals earning ₦800,000 or less annually are now entirely exempt from income tax, while top-tier earners making ₦50 million or more annually face an increased marginal tax rate of up to 25%.

Social safety nets have also been expanded, with the tax-exempt threshold for employment severance or injury compensation scaled up from ₦10 million to ₦50 million. Furthermore, a 20% rent deduction capped at ₦500,000 has been introduced to soften urban housing costs for workers.

For larger corporations and multinationals, the new regime tightens compliance and eliminates legal loopholes while simplifying the actual tax types.

In a massive bid to streamline corporate contributions, the government eliminated numerous separate, earmarked institutional levies—such as the Tertiary Education Tax (TET), NASENI levy, National IT levy, and the Police Trust Fund levy. These have been rolled into a singular 4% Development Levy charged on corporate assessable profits, greatly reducing accounting complexities. Additionally, the intermediate tax tier has been completely abolished, meaning businesses are now cleanly classified as either small (exempt) or standard corporate entities subject to the flat 30% CIT rate.

Previously, companies could exploit differences between the 10% Capital Gains Tax and the 30% Corporate Income Tax by creatively misclassifying trading income as asset disposal. The NTA closed this gap by raising Capital Gains Tax to 30% for companies. It also introduced indirect share transfer taxes, targeting offshore holding companies that flip assets derived from Nigerian property without paying local taxes.

To curb international profit shifting, large corporations with an annual turnover of ₦50 billion or more—or those belonging to multinational groups with global revenues exceeding €750 million—are now legally tied to a Minimum Effective Tax Rate (ETR) of 15% of their net income. If their real tax footprint falls below this, a top-up tax is applied, aligning Nigeria directly with global minimum tax principles.

While the headline Value Added Tax (VAT) baseline remains anchored at 7.5%, the inner mechanics underwent a massive correction. To combat inflation, the NTA broadened zero-rated protections for essential consumer items. Basic food items, medical products, educational materials, electricity generation/transmission, and public transport are protected from VAT.

Conversely, the digital economy has been reined in. Non-resident e-commerce platforms, streaming platforms, and international digital service providers are now legally mandated to register for, collect, and remit VAT directly to the NRS if they cater to the Nigerian market.

With the Federal Ministry of Finance enforcing its transition guidelines, the focus has firmly shifted to corporate awareness. Businesses across the country are navigating structural audits, adjusting accounting dates, and analyzing supply chain arrangements to ensure full adherence.

Ultimately, the tax reforms put in motion on June 26, 2025, represent a gamble on structural transparency. By trading short-term administrative adjustments for institutional clarity, lower burdens on small business, and stringent compliance for big industry, Nigeria is aiming to build a more predictable fiscal environment capable of driving long-term investment.